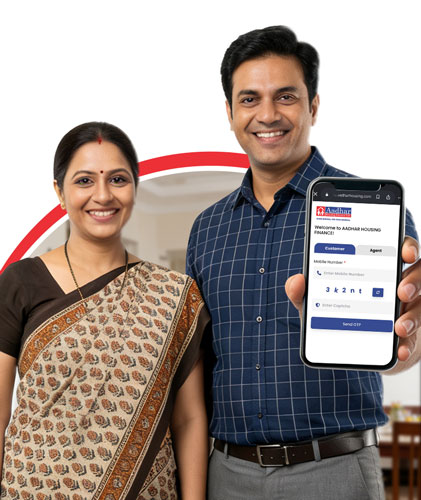

Finance for Every Brick of your Dream Home

Smart financing to help you build without compromise

3.15 Lakh+

Happy Families

600+

Branches across India

30,571 Cr

Assets Under Management

14 years+

of Trust & Service

We are proud to announce the opening of Aadhar Housing Finance's first All Women Branch in Delhi, taking our presence in the city to 24 branches. We are honoured to receive the Best HFC in Performance under PMAY (U) 2.0 – ISS award at the 2nd Housing & Housing Finance Excellence Awards 2025–26. We are proud to announce the opening of Aadhar Housing Finance's first All Women Branch in Delhi, taking our presence in the city to 24 branches. We are honoured to receive the Best HFC in Performance under PMAY (U) 2.0 – ISS award at the 2nd Housing & Housing Finance Excellence Awards 2025–26. We are proud to announce the opening of Aadhar Housing Finance's first All Women Branch in Delhi, taking our presence in the city to 24 branches. We are honoured to receive the Best HFC in Performance under PMAY (U) 2.0 – ISS award at the 2nd Housing & Housing Finance Excellence Awards 2025–26.

Home Loan Solutions for Every Need

Simple and affordable home loan options designed for salaried individuals, self-employed professionals, and first-time home buyers.

How we won the trust of 3.15 Lakh+ families of Bharat?

At Aadhar Housing Finance, we believe your hard work is your biggest credit score. We look beyond paperwork to help you build your home with an affordable home loan.

Inclusivity

No Income Proof? No problem. We assess your loan based on your actual earnings, making home loans accessible to everyone.

Massive Pan-India Reach

With 600+ branches in 22 states, our team is always ready to serve you whenever & wherever you need.

Transparent & Fast Process

Clear Terms. 100% trust. Enjoy a stress-free journey with zero hidden costs and quick loan approvals.

How To Apply for an Affordable Home Loan?

Follow these 4 simple steps to own your dream home:

Why Aadhar Housing Finance Limited Home Loans?

We make homeownership possible by looking beyond your paperwork to understand your real potential.

Know Your Loan, Before You Apply

Calculate your eligibility and EMI in one place to plan your home purchase with confidence.

Trusted by families across India

Real stories from families who trusted AHFL for their home loan journey.

After years of trying to buy a home, I faced rejections from financial institutions due to geographic limitations and low income. Approaching Aadhar Housing Finance was a different experience they guided me at every step, personally visited to complete the application, and ensured everything was in place. The entire process, from application to disbursement, was completed in just 15 days.

The company lived up to its name and provided Aadhar to me and my family in helping us buying our dream home.

After years of renting, buying a home seemed impossible as a cash salaried individual. But Aadhar Housing Finance made the process easy, ensuring everything was in place and approving my loan within 15 days. Owning a home is now a reality for me and my family, and we couldn’t be happier.

As a teacher, owning a home was my dream, but my loan applications were rejected due to my property’s Gram Panchayat location. Aadhar Housing Finance changed that by approving my loan in just 10 days, helping me become a proud homeowner. Recently, I took a second loan from them to buy another home, and the process was just as smooth. I’m grateful for their support and highly recommend them to anyone seeking housing finance.

Running a small pan shop for 17 years, owning a home felt like a distant dream. Aadhar Housing Finance made it possible with their timely support. Today, my family and I are proud homeowners, and I’m truly thankful to Aadhar.

We wanted to expand our house but struggled to get a loan as many institutions turned us down. Then, a family member told us about Aadhar Housing Finance. From our first visit, their team supported us at every step, helping us create the extra space we needed. Thank you, Team Aadhar!

I never imagined owning a home as a daily wage worker without an ITR. Aadhar Housing Finance not only helped me get a loan but also a government subsidy. Today, my life has improved, and I’m close to repaying my loan. I’m deeply grateful to Aadhar.

After struggling to get a loan for 10 years, Aadhar Housing Finance supported me at every step of the process. Their team was accommodating and made my home loan journey easy. I am deeply grateful and highly recommend Aadhar.

Owning a home always felt like an impossible dream for us. We weren’t sure if we would qualify for a loan, but the Aadhar team changed everything. They listened to our concerns, understood our needs, and guided us with constant support. Today, we are proud and grateful to be the owners of our dream home, all thanks to Aadhar!

Being a small businessman, I wanted to build my own home on my own land. But I was facing rejection at every step. A relative asked to me approach AHFL. The team helped me from the scratch and ensured that I built the home of my dreams just the way I dreamt.

I own a small bakery and struggled to get a loan for business expansion, facing rejection everywhere. A friend suggested Aadhar Housing Finance, and to my surprise, they approved my loan despite limited documentation. Thanks to AHFL, I’ve successfully expanded my business. I’m truly grateful to the team for their support.

I owned a flat yet I wanted to build a home of my own. My application was rejected by multiple institutions due to low income. A friend told me about AHFL. With their prompt help, I was able to build my own home in just 3 months. I invite the AHFL Team to be a part of my new home’s housewarming ceremony on 11th Dec 2024.

Learn, plan, and borrow smarter

Easy guides, tips, and tools to help you understand home loans, eligibility, EMIs, and everything in between.

01 Aug 2024

01 Aug 2024Loan Against Property Without Income Proof in India

Discover how you can leverage your property's value to secure funds even without standard income documentation. A perfect solution for business owners and freelancers.

Read Full Article